MN Mortgage Matchmaker: Find the Best Home Loan for You

You are executing the preparation playbook. You are managing your debt, you are mastering your budget, and you are building true Financial Wellness. You have confirmed your Buying Power, a critical play we explain in [The Simple Math of a MN Home Loan: Understanding Your DTI | Knowledge Center].

But now you are facing the biggest, most confusing array of choices. You hear people talk about "Conventional" loans. Then you hear "FHA." Then "VA." Then "USDA." You hear about special programs, and you hear that one neighbor got a great deal that your other neighbor couldn't qualify for. This overwhelming choice creates massive anxiety, which fuels a lingering doubt. You are thinking: “Which loan should we get?” “What if we choose the wrong one?”

I need you to stop thinking that way.

At CirclePartnersMN.com, we approach the Central Minnesota housing market with education first, absolute empathy for the challenges you face, and a goal to make this process tremendously engaging. We know that the choices are confusing. But we also know a powerful, strategic huddle play: Mortgage Matchmaking.

A home loan (a mortgage) is not "one size fits all." It is a strategic tool. There are different loan "programs" (created by different government agencies or private companies), each designed for a specific type of buyer with different financial situations and goals.

In this guide, I am going to give you the exact tactical steps to understand the four main loan types, audit your situation, and find your perfect mortgage match to unlock your future in a Minnesota home.

Part 1: Your Action : Finding Your Local Partner

Before you can match with a loan, you must partner with the right matchmaker. A core philosophy of our [Partner With Us | Knowledge Center] is that you need a guide, not a website.

Your Action: In your huddle, you must partner with a Reputable, Local Minnesota Lender (a bank). This is why a core play in [The Minnesota Pre-Approval Playbook | Knowledge Center] is to avoid national online dot-com lenders. A local lender:

Knows the local rules, taxes, and unique Minnesota mortgage environment.

COMMUNICATES better with local listing agents, adding trust to your offer.

Is often much faster and more responsive when you have an urgent question.

When you start your pre-approval process, you aren't just giving documents. You are building a relationship with an expert whose job is to audit your financials and recommend your strategic loan match through the buying process and beyond.

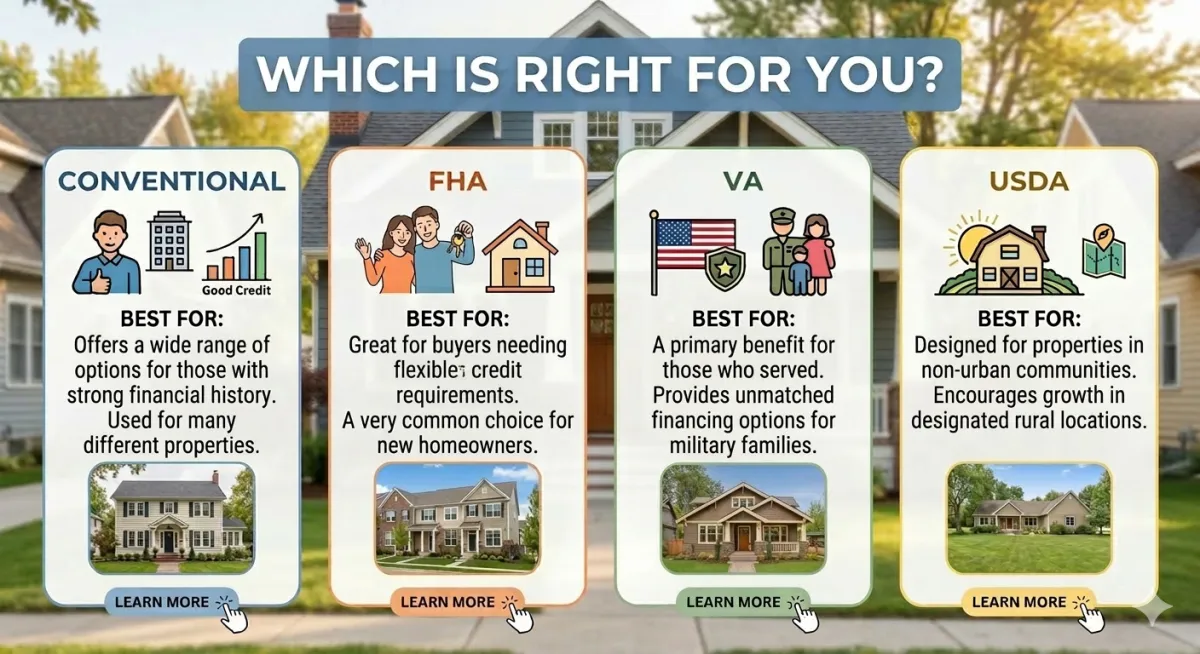

Part 2: The 4 Primary Loan Types

There are 4 main types of Loans. Each program has different rules for your credit score, your Debt-to-Income (DTI) ratio, and your down payment required, and in some cases the home you want to buy.

1. Conventional Loans (The Standard Play)

This is the standard play. Conventional loans are not backed by the government. Instead, they follow rules set by two large private companies, Fannie Mae and Freddie Mac.

Credit Score: Higher requirements (often 620–660 minimum). A better score gets you much better rates, a concept we explore in [Minnesota Credit Revival | Knowledge Center].

DTI Ratio: Generally stricter (max 43%, sometimes higher with a strong score).

Down Payment: Many buyers mistakenly believe 20% is required, but the reality is as little as 3% for qualified buyers!

The Match: A conventional loan is a great match if you have stronger credit (700+) and a stable DTI. It offers flexibility and is highly respected by sellers in cities like Edina and Plymouth. We explain the detailed roadmap and pitfalls to avoid in [Navigating MN HOA Life: Townhomes, Condos, and What You Need to Know | Knowledge Center].

2. Federal Housing Administration (FHA) Loans

This play is designed to make homeownership accessible. FHA stands for the Federal Housing Administration. The FHA insures the loan, which means the government is protecting the bank if you stop paying. This makes the bank willing to offer easier terms.

The Strategy Audit:

Credit Score: Much more lenient (can go as low as 580 with a small down payment, sometimes 500 with a larger one). This is an empathetic option if your Credit Revival is still in progress.

DTI Ratio: Much more flexible (can go up to 50%, 55%, or even 57% in rare cases!).

Down Payment: A fixed 3.5% minimum.

The Match: An FHA loan is often the perfect match for first-time homebuyers in Minnesota, or for buyers with lower credit scores (580–660) or a higher DTI. This program allows you to execute your Buying Power strategy, a concept we cover in [How To Buy a Home in Minnesota | Knowledge Center]. FHA loans are common across Central MN, from Brooklyn Park to St. Cloud.

3. VA Loans (The Veteran’s Play)

This play is specifically for our veterans, active-duty service members, and eligible surviving spouses. The Department of Veterans Affairs (VA) guarantees these loans, making them the most powerful loan option available. We take immense pride in supporting our MN veterans in [Leaving Your Legacy in Minnesota | Knowledge Center].

The Strategy Audit:

Credit Score: Lenient (often no official score required, but lenders typically look for 620).

DTI Ratio: Incredibly flexible (no strict limit, often 50%+ is allowed).

Down Payment: 0%! ZERO PERCENT DOWN! This is the ultimate power play.

NO Mortgage Insurance: Every other low-down-payment loan requires you to pay "mortgage insurance" (a monthly fee). VA loans do not.

The Match: If you are eligible, a VA loan is almost always your best match. Period. It provides the best rates, the lowest costs, and allows you to preserve your cash for building wealth and enjoying being [At Home in Minnesota | Knowledge Center]. We are committed to educating veterans across Central Minnesota on this powerful, earned benefit.

4. USDA Loans (Rural Development)

This play is for buyers in rural areas. The U.S. Department of Agriculture (USDA) guarantees these loans to promote stability and growth in smaller MN towns.

The Strategy Audit:

Credit Score: Lenient (often 640 minimum).

DTI Ratio: Strict (max 41%, can be slightly higher with a strong score).

Down Payment: 0%! ZERO PERCENT DOWN! Another powerful 0%-down play.

Location Required: The home must be in an eligible "rural" area. This means you cannot use it in major cities like Minneapolis or Bloomington, but it is a powerful play for smaller, thriving MN towns like Buffalo, Zimmerman, or parts of Big Lake.

The Match: A USDA loan is a great match if you have a lower DTI, a stable income, and you are looking for that perfect, quiet, non-urban life in Central Minnesota. It turns that impossible mountain into a climb you can execute with strategy, a central philosophy of [MN Financial Wellness: Your Plan to Save | Knowledge Center]. We are dedicated to educating rural Minnesota communities on this specialized wealth-building tool.

Ready to Huddle Up? Let’s Execute the Playbook.

At CirclePartnersMN.com, we understand that choosing a home loan is terrifying. That’s why we approach the Minnesota market with education first, absolute empathy for the massive life transition you are making, and a dedication to making this process tremendously engaging.

A home loan is not "one size fits all." It just requires a powerful huddle play. State-sponsored down payment assistance is not a handout; it is a tactical tool. It is the tactical decision that moves you from being an anxious, speculative shopper into a strategic, empowered MN homebuyer.

You don't have to build your strategy alone. We are here to answer your questions, guide you through this Preparation phase, and connect you with trusted local lending partners who are absolute experts in building custom affordability plans that utilize these powerful state programs.

Don’t let anxiety or a confusing math stop your vision of your future. Start your audit. Start your DPA strategy. Start your journey today.

Your Loan Strategy Starts Here.

Contact CirclePartnersMN.com today. Schedule your consultation, and we will answer all your questions about loan types, preparation, and your future in a Minnesota home.